Are We In a Housing Crisis?

The affordability problem continues

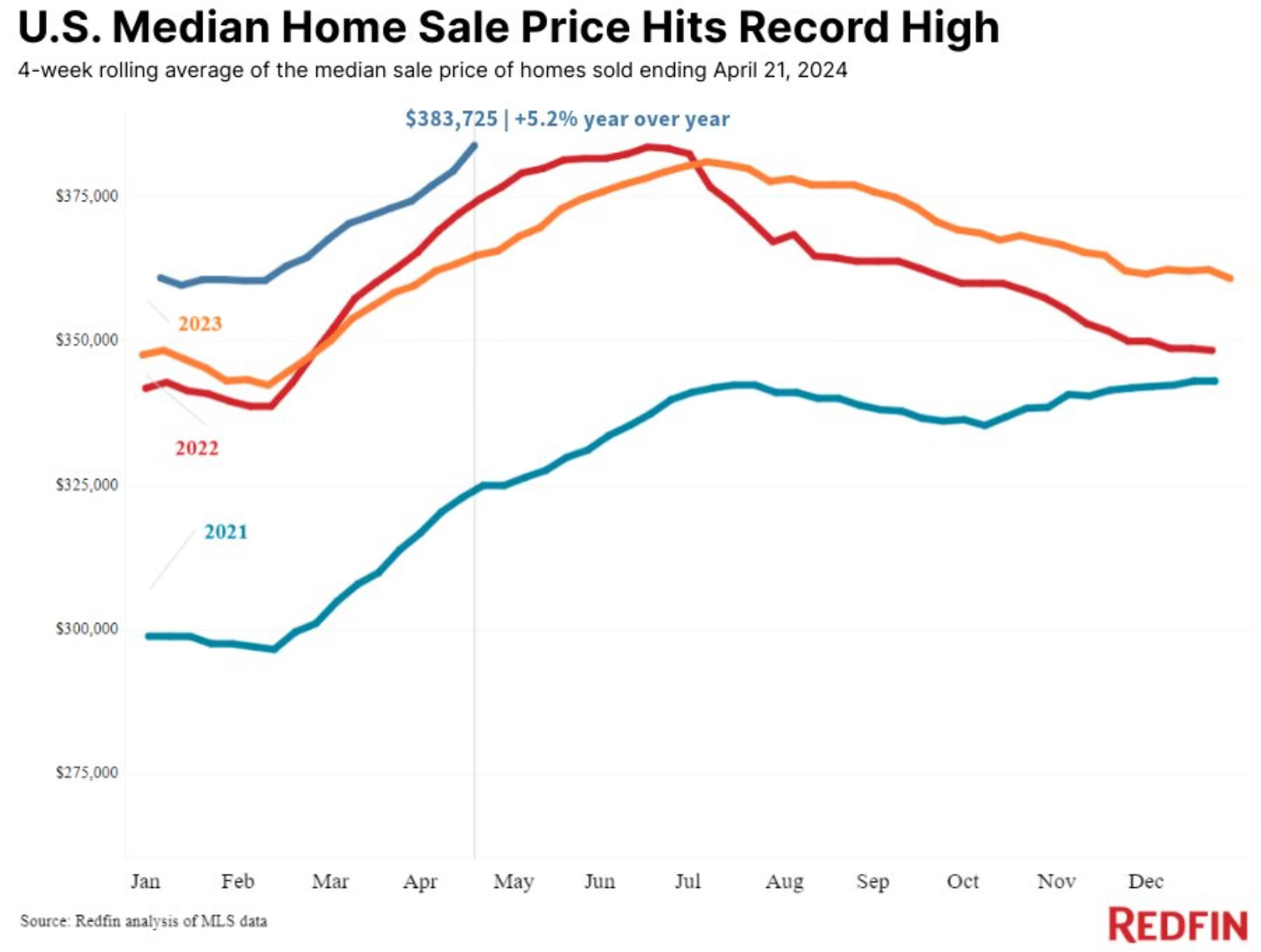

The median U.S. home sale price just hit a new record high of $383,725.

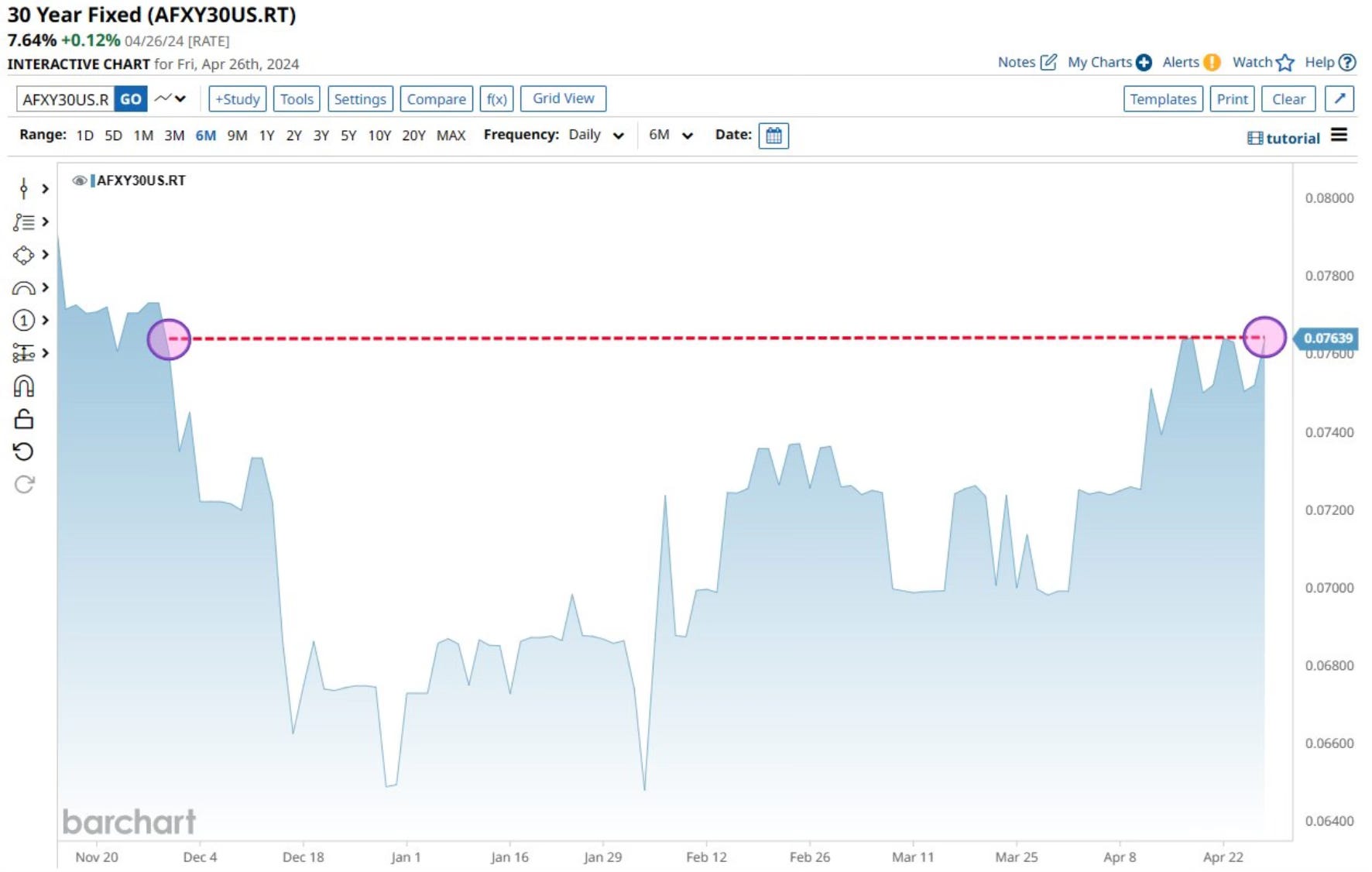

This record high sales price was set while mortgage rates hit their highest level since November 2023. The 30-year mortgage is now at 7.64%.

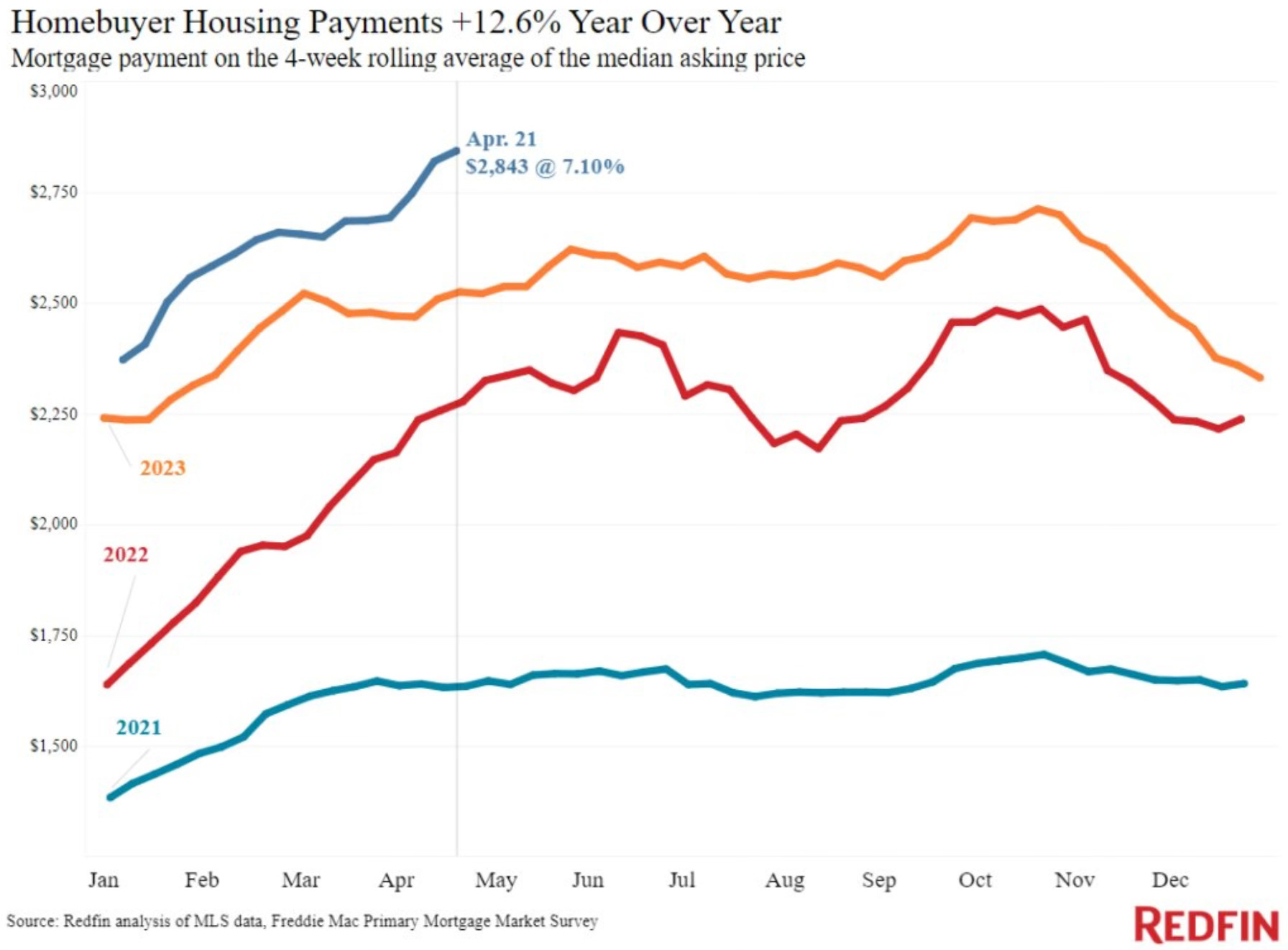

The combination of record high prices and high mortgage rates have drove the median monthly housing payment to a record $2,843. Now up almost 13% year over year.

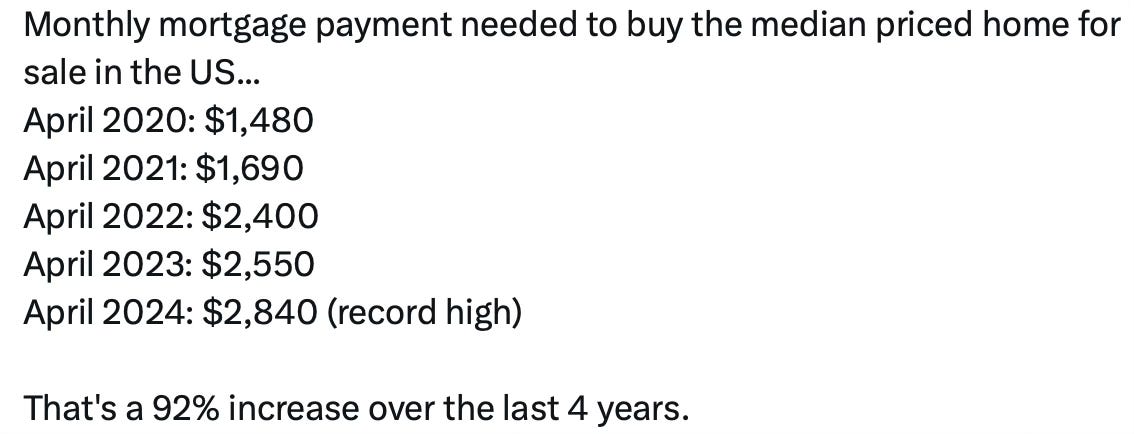

Home affordability sits at an all-time low. Let’s look at the number to see just how much it has changed. This was a good visual from Charlie Bilello showing how much the monthly mortgage to buy the median priced home in the U.S. has changed from April 2020 until April 2024. Up 92% in 4 years!

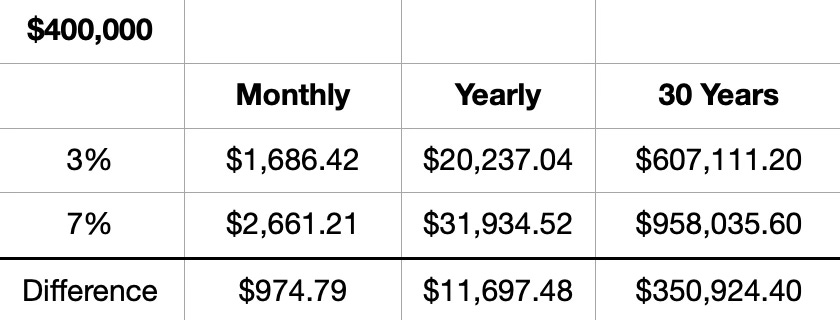

I decided to run the numbers on how that would impact a $400,000 mortgage. I compared what the mortgage payment would have been four years ago at 3% and where it would be now figuring a 7% mortgage.

Then I took the overall cost difference per month, yearly and over the 30 years of a mortgage. Look at the difference!

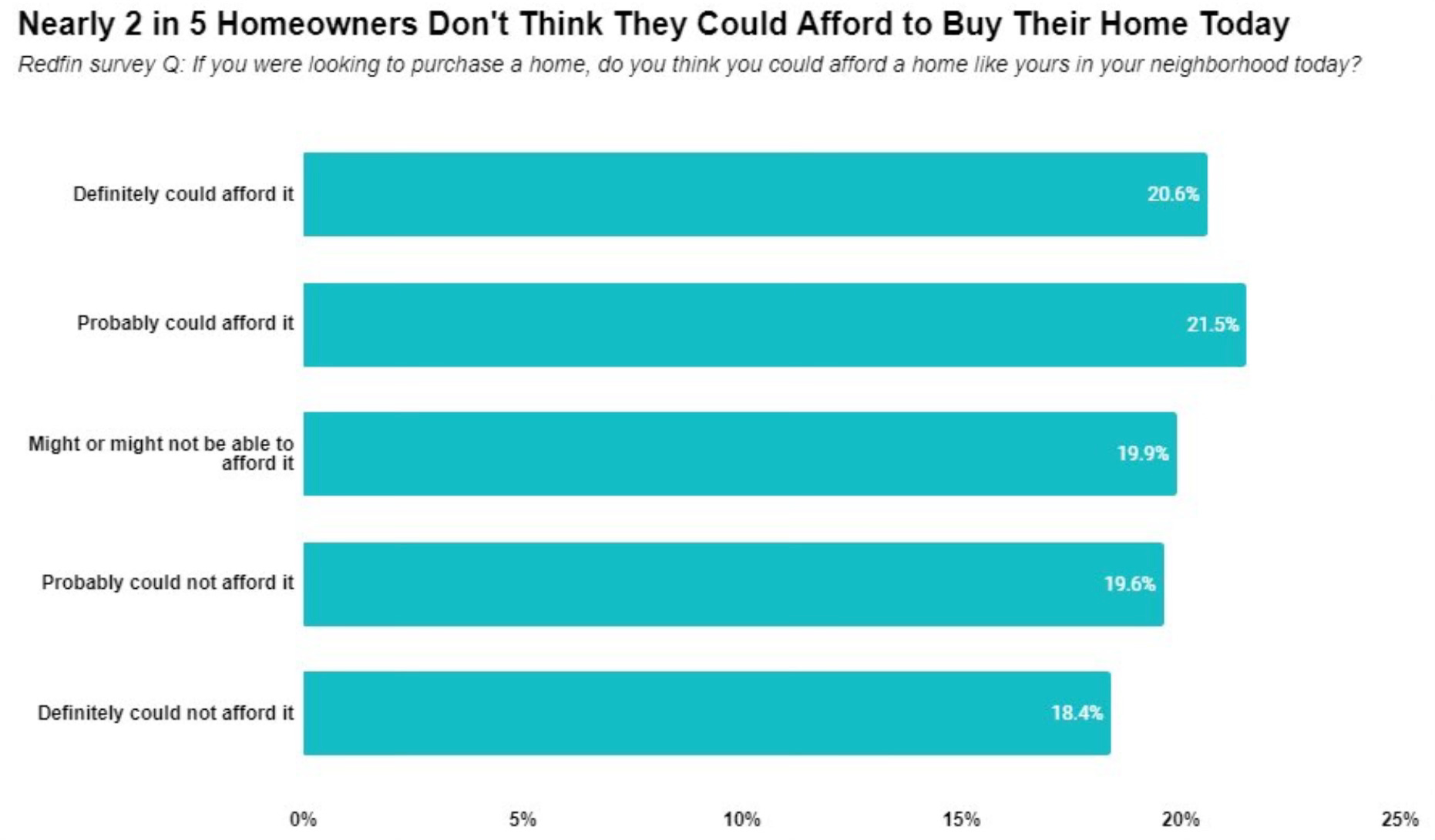

Once you see these numbers you can understand the responses to this survey from Redfin. They asked if you were looking to purchase a home, do you think you could afford a home like yours in the neighborhood today? 2 in 5 or 38% don’t think they could.

We built our home back in 2018. I had my builder estimate the cost to build it today and it would be double the cost. The mortgage rate on our home is 3%. If we were to build today, our home would cost twice as much and our mortgage would be around 7% instead of 3%.

This is a common story from many. Why would anyone want to move or trade up in a home unless it was absolutely necessary? If you have a locked in mortgage rate of 3% or less, you have won the lottery.

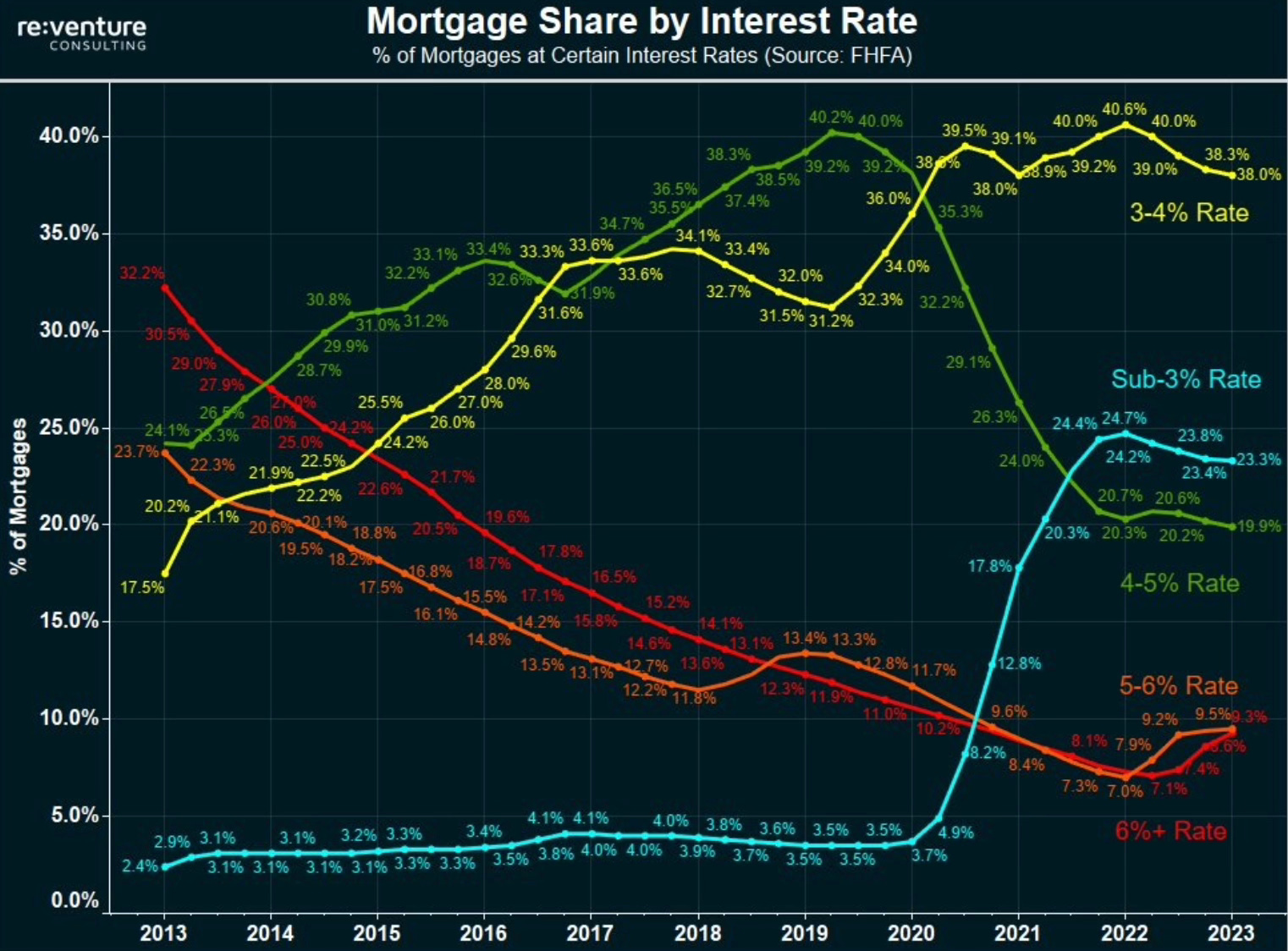

Here is a breakdown of the percent of outstanding mortgages at certain interest rates. 23% of all outstanding mortgages have an interest rate under 3%. 61.3% have an interest rate under 4%.

Will we see those low of rates again? Not anytime soon. Many probably won’t again in their lifetime.

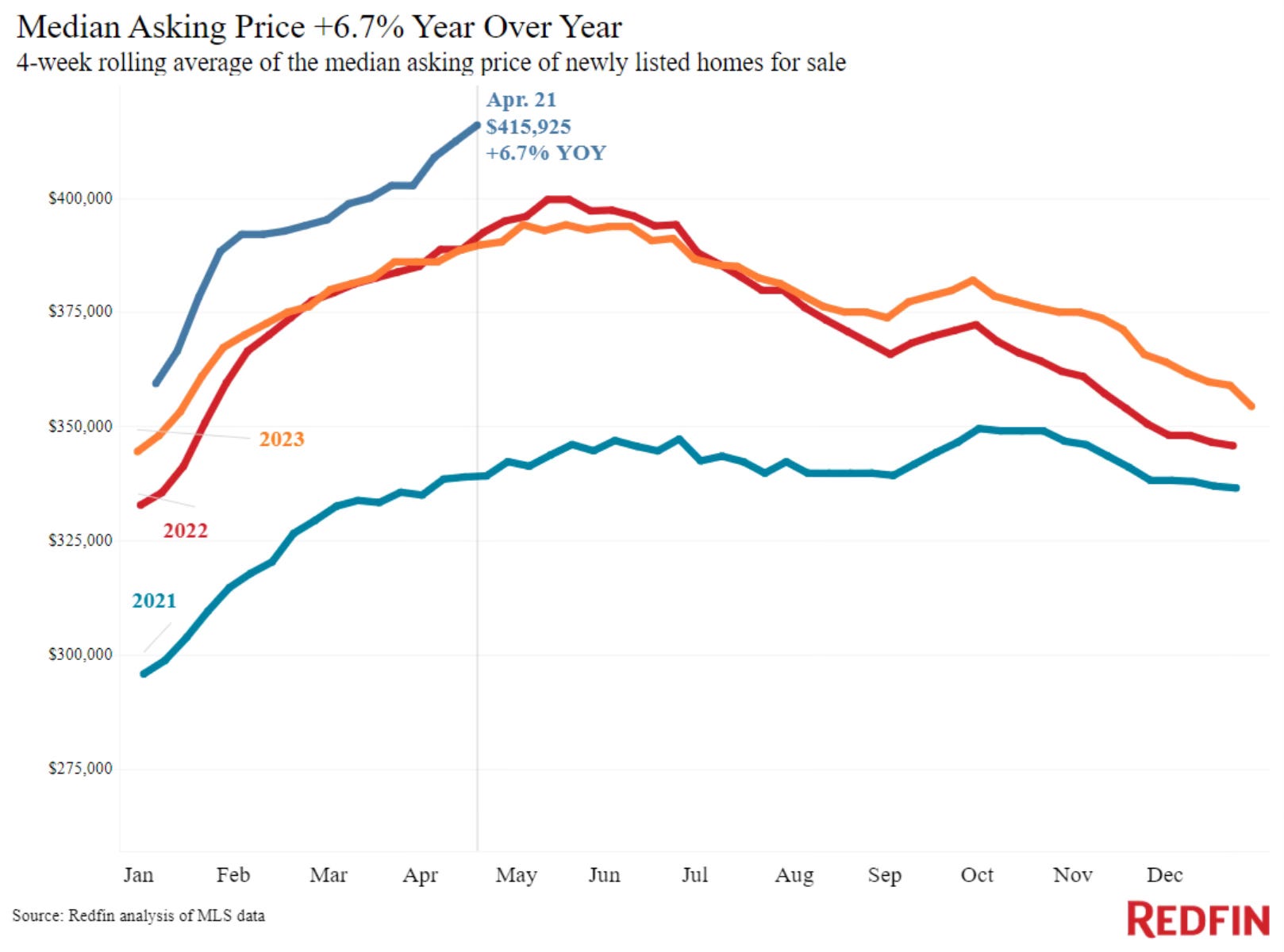

Despite all of this, the median asking price of homes continues to also climb. It’s at an all-time high of $415,925.

The raising of interest rates couldn’t slow the housing market. Rate rose higher, but so have prices. “Can’t afford a house” or “Can’t afford to move” are true and accurate phrases to describe the current state of housing.

The Fed raised rates which slowed supply and sales but not demand and prices.

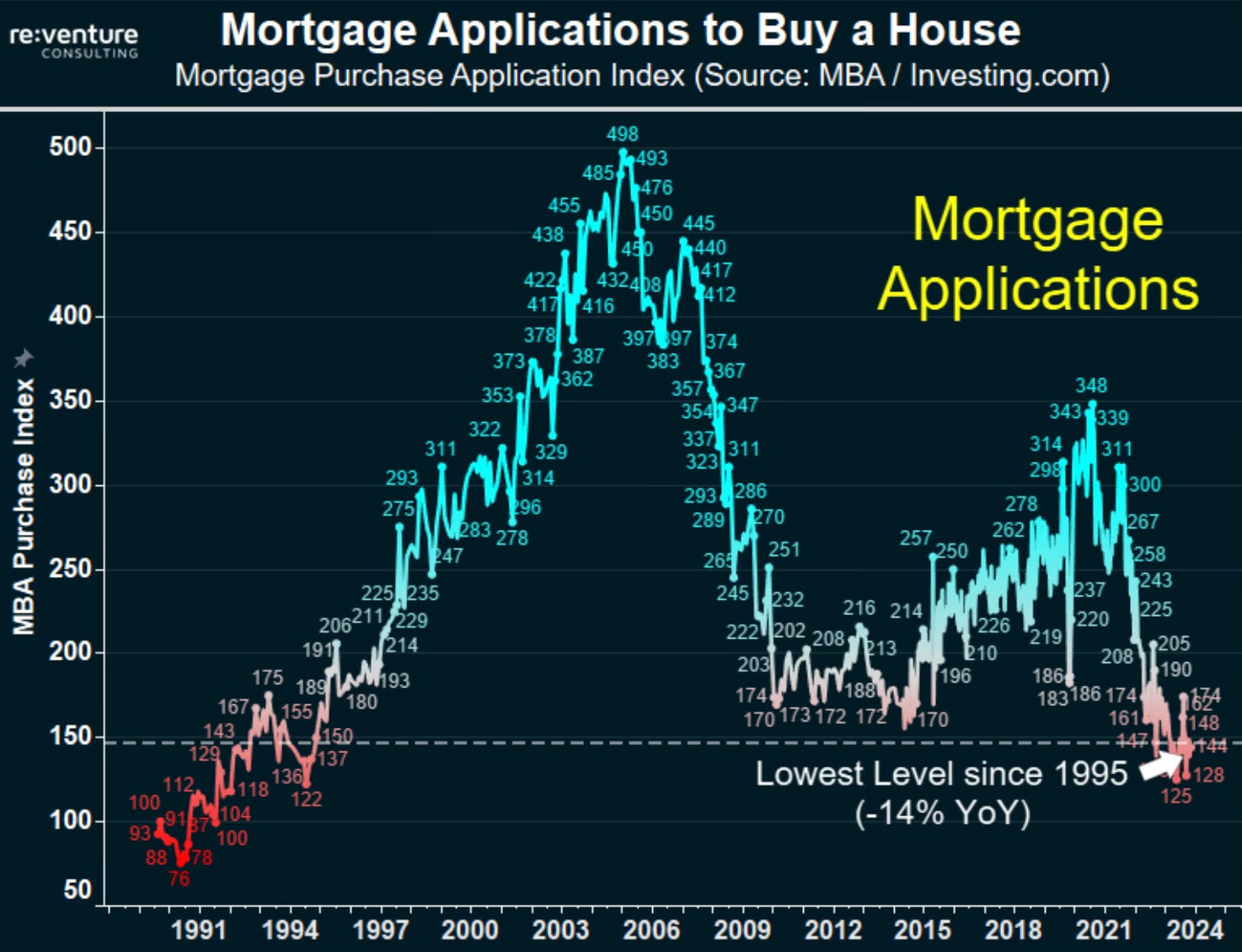

It has created what I would characterize as a housing crisis. First time home buyers are in a terrible position. They have record high home prices along with multi decade high mortgage rates. That translates to record low affordability.

Demand for homes remains high. There simply isn’t enough inventory of home for sale to meet demand.

Unless first time home buyers receive help from parents or receive an inheritance, they’re really facing an uphill battle.

Is there a solution to this housing affordability crisis? That’s a question that has been running through my mind for months.

I don’t believe the Fed can get us out of this. They can’t lower rates. Could you imagine what would happen to prices if mortgage rates lowered into the 5-6% range? Home prices will skyrocket even higher.

Could they raise rates even higher? That could slow home sales to a literal standstill and that runs the risk of something braking causing a bigger problem.

Does some form of a first time home buyer program come back?

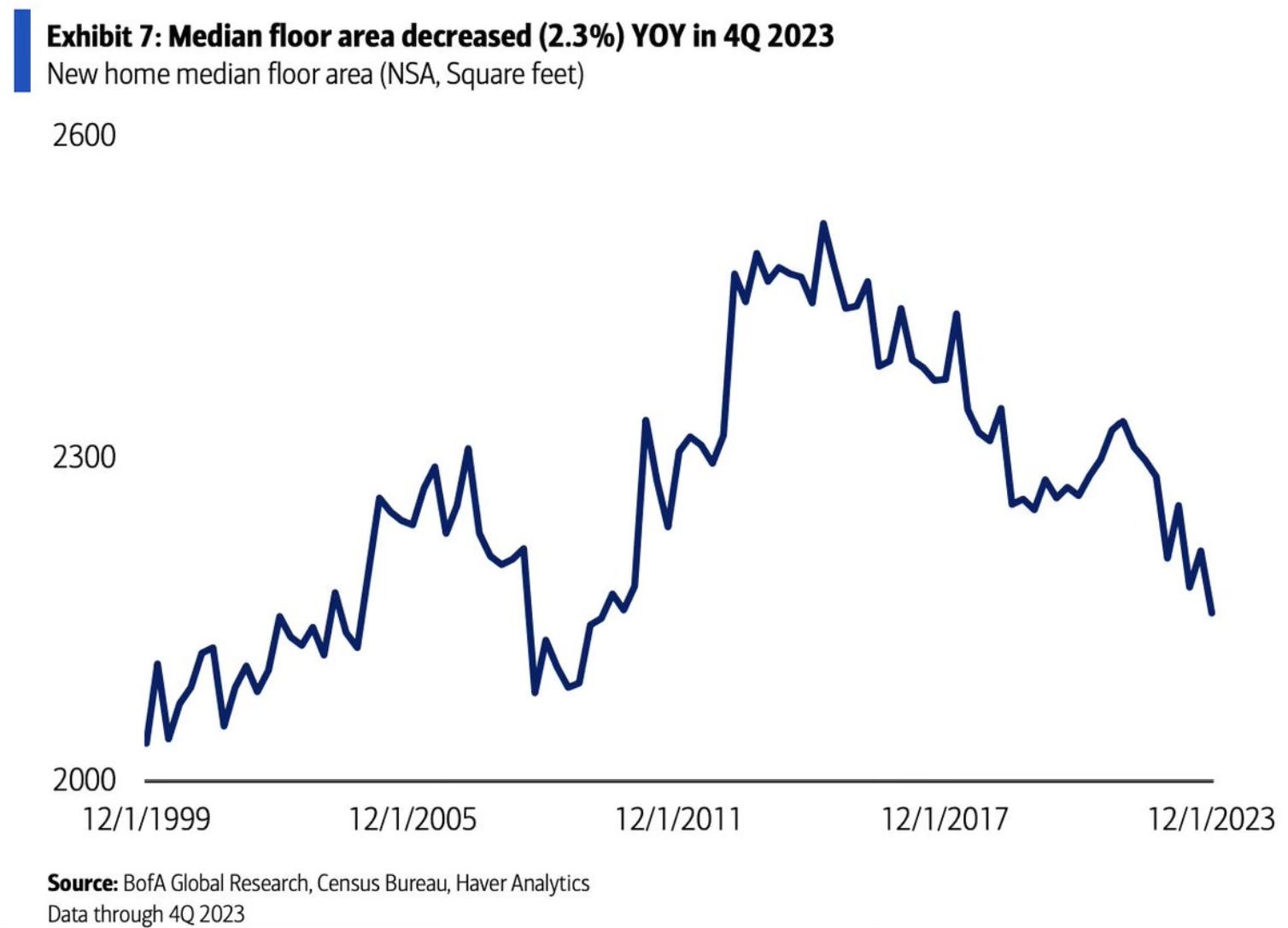

Home builders have been able to buy down mortgage rates and offer other incentives to keep moving homes. They have begun to decrease the size of homes they build to accommodate the affordability problem.

But a not so good sign for builders is that lumber futures have turned much lower. This usually indicates that there is a slowing demand for new homes. Higher rates and affordability may also be catching up to the home builders as well.

Over the coming months I feel that housing and where this home affordability crisis leads is one of the more important story lines about the economy to watch.

Home prices, as well as mortgage rates will remain elevated. There is nothing to suggest otherwise anytime soon.

So where does this road lead? Your guess is as good as mine. We will all be along for the ride.

The Coffee Table ☕

Nicole Friedman of the WSJ had a good piece called The Hidden Costs of Homeownership Are Skyrocketing. This was a very good article about what homeowners are facing with the rising costs of insurance, property taxes and maintenance costs. The bad part is that it doesn’t look to be getting any better. Likely only worse.

Ben Carlson wrote a good post on housing called Who is Buying a House in this Market? He looks at the age of home buyers and their incomes. There is a lot of interesting demographics in here of what’s making up the home buyers.

Thank you for reading! If you enjoyed Spilled Coffee, please subscribe.

Spilled Coffee grows through word of mouth. Please consider sharing this post with someone who might appreciate it.

Order my book, Two-Way Street below.