Inflation Affects All of Us

Inflation Affects All of Us

What you should know and what you can do

If there is one thing that touches every consumer and business in this country, it’s inflation. You can’t escape the word or the headlines in almost every story you read or watch.

I knew about inflation and how it works, but it has never been a problem to worry about in my lifetime. Now in 2022, it has returned to its highest levels in 40 years. I decided to research and educate myself further on inflation. Here is what I learned.

What Is Inflation?

Inflation is the decrease in the purchasing power of money. Your dollar will not go as far in the future as it did today. This means that the price of goods and services is rising.

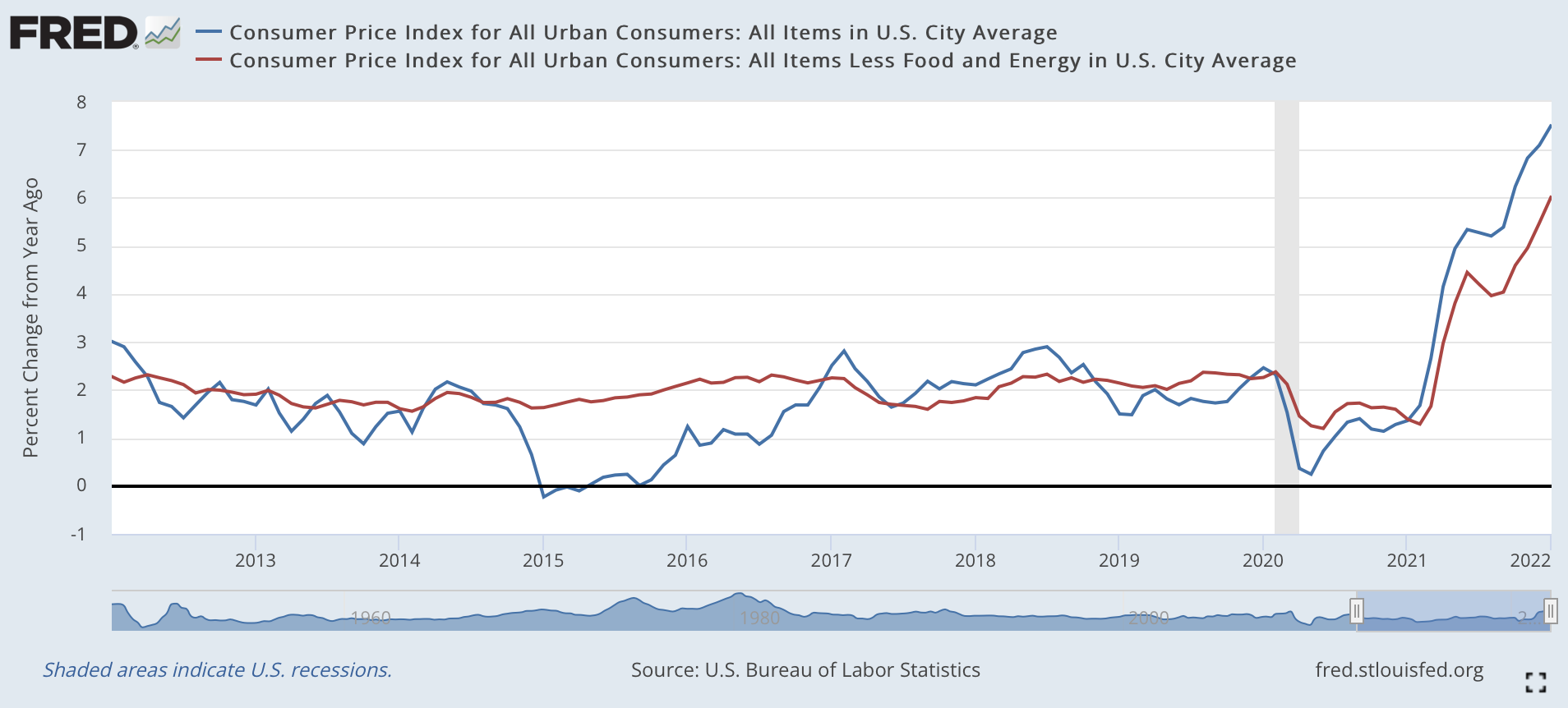

There are two ways inflation is measured. The Consumer Price Index (CPI) is the overall measuring stick of inflation. Often referred to as headline inflation. It’s the measure of the average change in the prices paid by urban customers for a basket of consumer goods and services.

The second is the CPI number minus food and energy. This is often referred to as the core inflation number. Food and energy prices are removed due to their high volatility.

Why Did It Rise?

This rise in inflation can be attributed to a hot economy. After the flush of goverment stimulus money hit consumers pockets, they were flush with cash. You had the stock market and cryptocurrencies at all time highs. Home values also at all-time highs. Credit became easily accessible.

The demand picked up and people were ready to spend. In fact, consumers have been on a spending spree and have not slowed up.

Spending came roaring back as many companies were slowed or even shut down due to the pandemic. So inventories and supplies were wiped out. Companies were able to start ramping up production again. But many forget that a lot of businesses were completely shut down. General Motors and 3M changed their shut down factories to making ventilators during the Pandemic shortage in 2020.

There were a large number of workers that were laid off. Companies had to get workers back and restart production again. In many cases the workers never came back, or changed job. This has created an uptick in wages and the fight for workers has come down to who can offer the most money, resulting in wage inflation across the country.

We’ve all seen and heard about the issues with the port congestions and truck driver shortages, so the delivery of goods has been delayed. Thus resulting in supply and demand constraints.

The pandemic really screwed up supply chains and caused labor shortages. Consumer demand and supply constraints continue to push prices higher. Should any of us really be surprised we have these high levels of inflation?

Will It Continue?

Prices are not going to go back down to pre-covid levels. If inflation does tick down, do you see companies reversing and reducing prices? We all know the answer to that. Companies are going to protect margins and their bottom lines.

January’s biggest gains in inflation were food, electricity and shelter. A recent Gallup poll in Barron’s showed that 8 in 10 American expect inflation to rise.

If any companies have a read on what inflation is doing to their business as well as consumers, it’s the consumer packaged food companies. Here is what executives at Kellogg and Tyson Foods said recently on inflation.

Kellogg’s Chief Financial Officer Amit Banati said the following Feb 10th.

“In terms of inflation, I’ll start there. It’s continued to accelerate, and we’ve seen that through 2021. So we are expecting double-digit inflation in 2022, and the bulk of it is market-driven…We’re seeing inflation in ingredients and packaging, oil, corn, wheat, and on the packaging side, cans, cartons. So we’re seeing broad-based inflation across our ingredients.”

Tyson Food’s Chief Executive Donnie King said the following on Feb 7th.

“We have seen a lot of inflation…Labor costs have been up 20%, cattle costs are up—have been—they’re up 22%. Grain has been up 29%. This year in freight, I mentioned earlier, is up 32%. We’re not asking customers or the consumer ultimately to pay for our inefficiencies. We’re asking them to pay for inflation.”

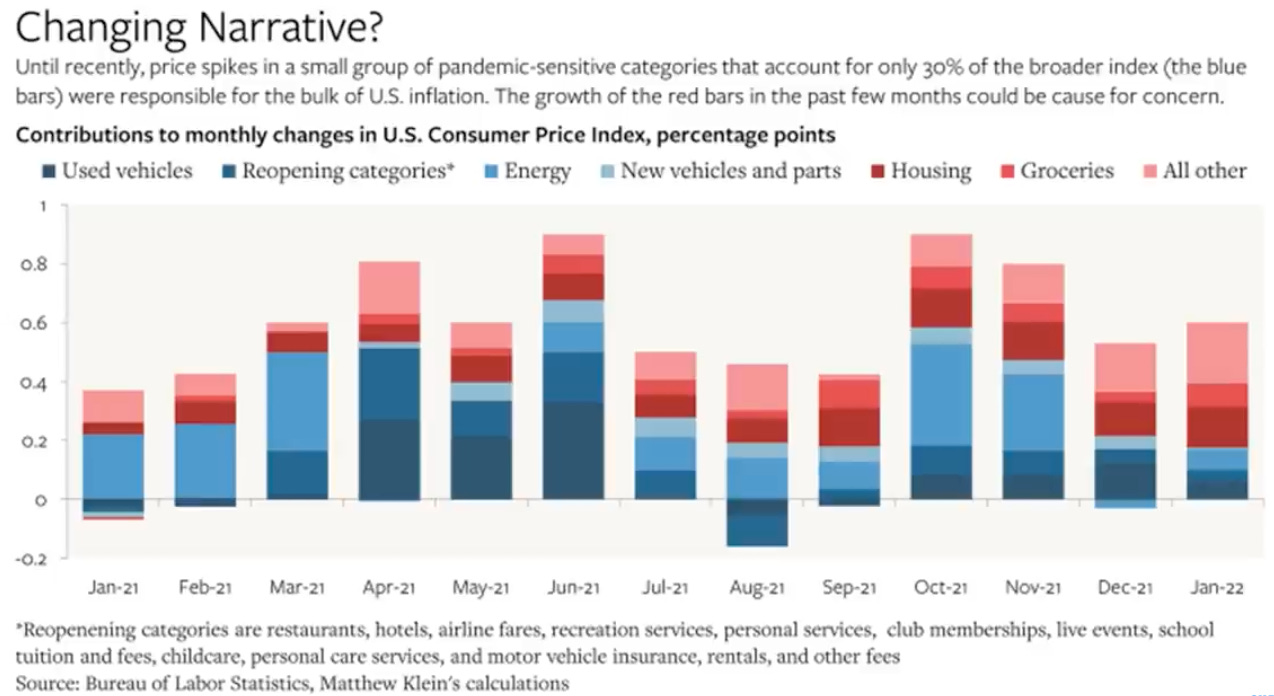

Matthew Klein on his Substack The Overshoot, had an interesting chart that shows a shift in what categories have been rising of late, which could be cause for concern.

The WSJ had a story on economist Mickey Levy of Berenberg, in which they summarized his concerns.

Economist Mickey Levy of Berenberg has scrutinized data for more than 200 individual goods and services for which the government tracks prices. An increasing number of individual items are subject to higher rates of inflation, he warned on these pages in December.

His update based on last week’s data suggests the problem is growing worse. Some 73% of the items saw annual price rises of 3% or higher in January, and some 55% of items saw inflation of 5% or higher. Keep in mind the Federal Reserve’s inflation target is 2%.

What You Can Do

Costs have risen and been added to every step from production to sales, resulting in higher prices. Rising prices cause hardships for families. According to this WSJ article, higher inflation is probably costing you $276 a month.

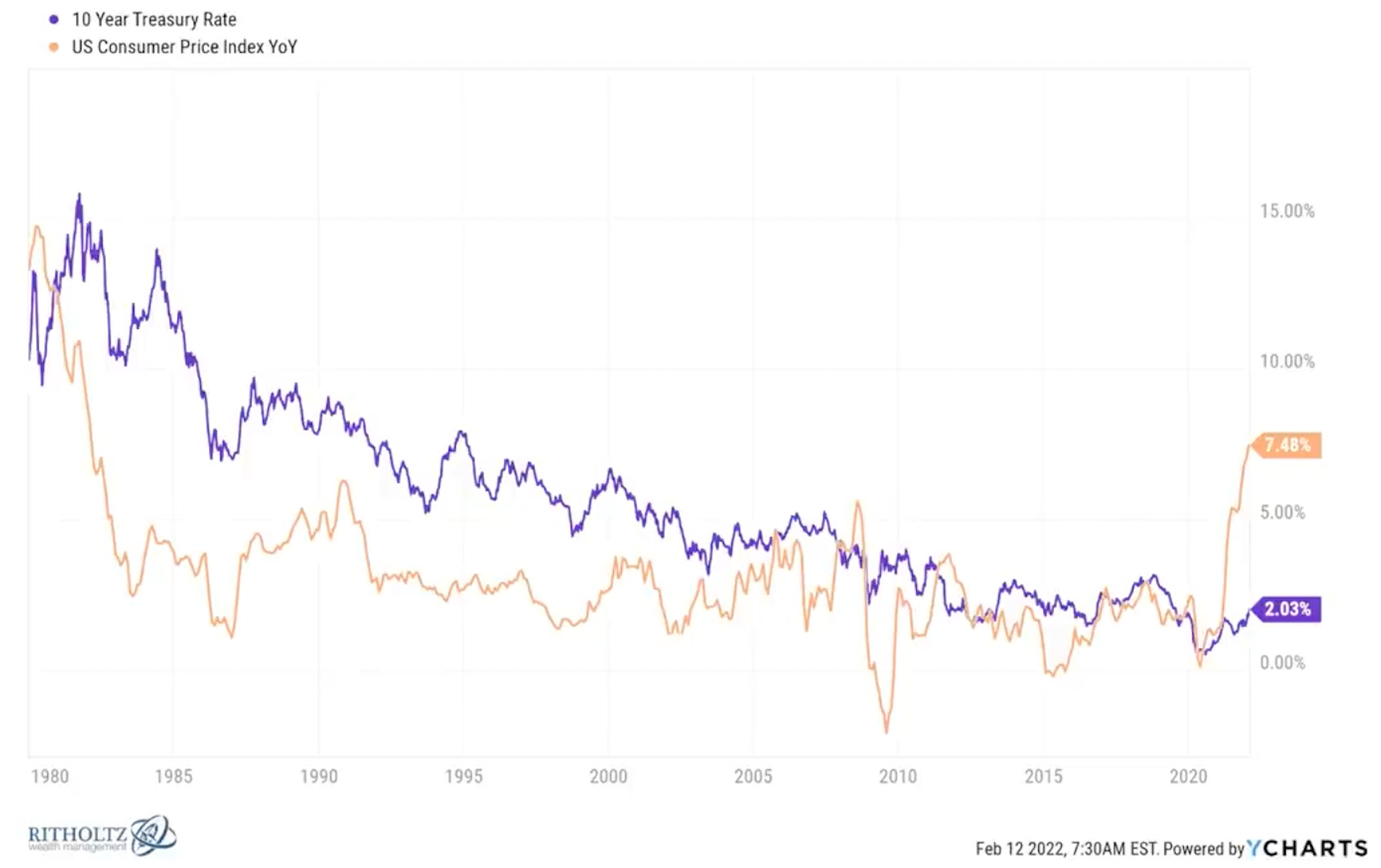

Inflation tends to sap spending and consumer confidence. Higher mortgage and interest rates usually follow. It seems you’re paying more for everything.

Mortgage rates for the week ending February 17th.

One way to stay ahead is to be sure you have any unsecured debt locked in. Lock in rates long term on mortgages, refinances or HELOCs. Homes, student loans debt, business financing etc. Contact your financial institutions and see what the interest rate setup is. If you still have any ARMs or adjustable rates on anything, lock in the rates for the long term. This will protect you as rates start rising and save you money in the long run.

If you have been holding off on spending on something, consider doing it now. Does anything ever really get any cheaper than to just do it now? If you’ve ever done any improvement to your property (renovation, addition, finishing a basement, garage, deck, patio etc.) you know doing it now is always cheaper than waiting because the costs just rise.

I’ve spent four years considering adding a whole house generator. Every single year I’ve checked it has got more expensive. What started around $8,000, has now gone up to $14,000. I kick myself for not doing it four years ago. I’ve decided on doing it now. I know it only will get more expensive.

Fed officials think the surge in inflation will ease later this year. We can all hope that is the case, but our bills will do the talking and tell us whether that happens or not.

Thank you for reading! If you enjoyed Spilled Coffee, please subscribe and/or give a gift subscription for others.

Spilled Coffee grows through word of mouth. Please consider sharing this post with someone who might appreciate it.