Why Are Mortgage Rates Rising?

What it means and why it's important

As the Fed started to cut interest rates last month, the expectation was that mortgage rates would fall.

What many don’t understand is that the Fed doesn’t set mortgage rates. They can influence mortgage rates, but they don’t set the rates.

Mortgage rates are heavily influences by the 10-Year Treasury Yield.

The 10-Year Treasury reacts to the outlook for economic growth and inflation.

With the economy still showing strength, a solid job market and rising long-term inflation expectations, the 10-Year Treasury has gone up.

It’s up to 4.20%, the highest level since July.

Since the Fed cut rates by 50 bps, the 10-year has headed straight up, not down.

As the 10-Year has risen, so have mortgage rates. The 30-Year Fixed Mortgage is now at 7.26%. That’s the highest level since July and marks the 4th straight week of increases. The recent low was 6.11% in August.

You can see that since the Fed started to cut rates, the 30-Year Mortgage rates have gone straight up as well. It’s the opposite of what everyone thought would happen.

As mortgage rates have remained high, combined with record low affordability, it should come as no surprise that home sales have struggled.

But it’s actually much worse than I thought. Data from Redfin shows that minus the pandemic, the closed sales of existing homes in September actually dropped to the lowest level since 2012.

Mortgage applications fell 17% last week. That’s the largest weekly drop since April 2020.

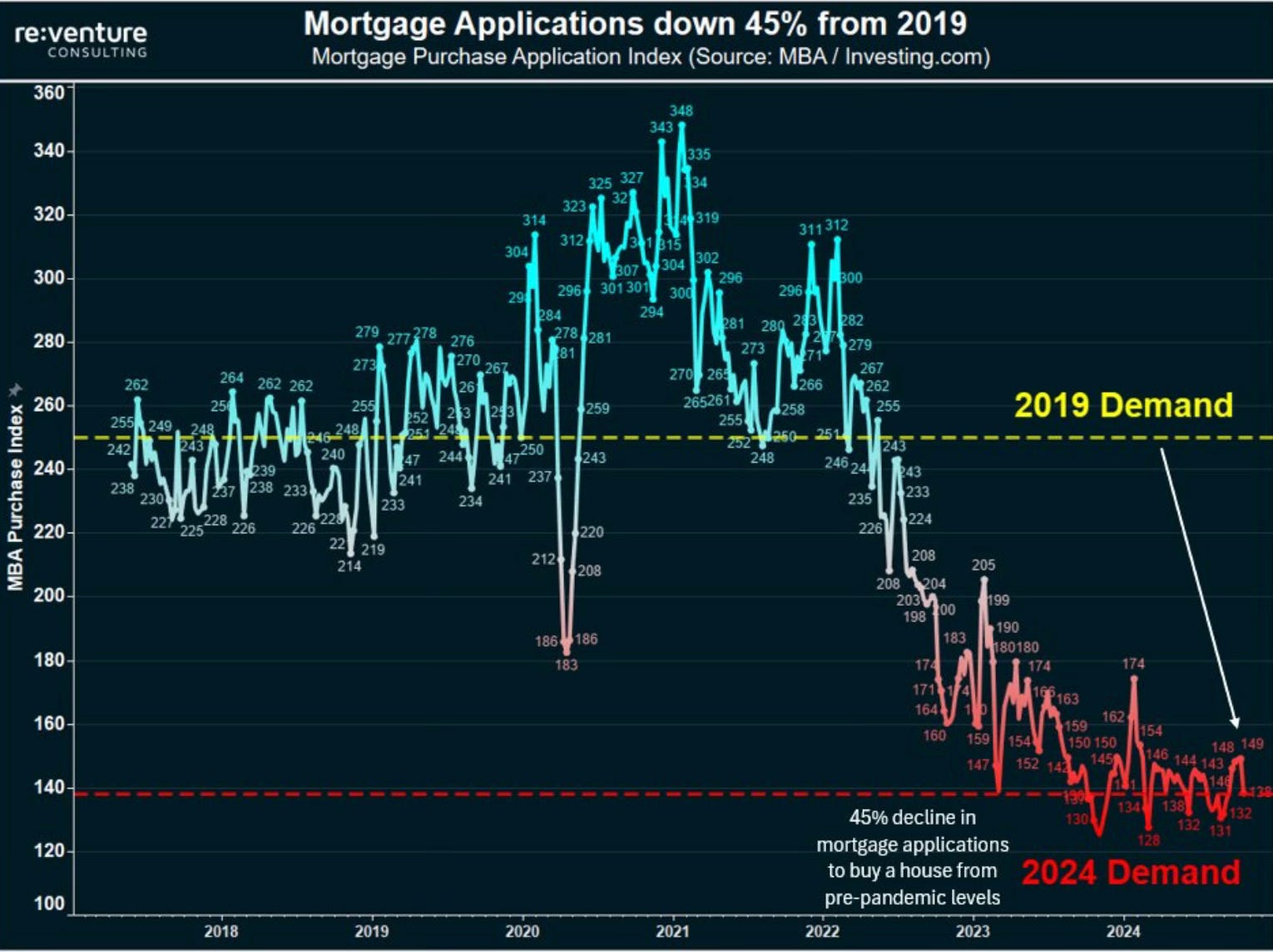

Mortgage applications are actually down 45% from 2019.

This is some worrisome data when everyone was waiting and expecting mortgage rates to go down as the Fed started to cut.

Since the opposite happened and rates rose, what happens next and why is housing activity so important to the overall economy?